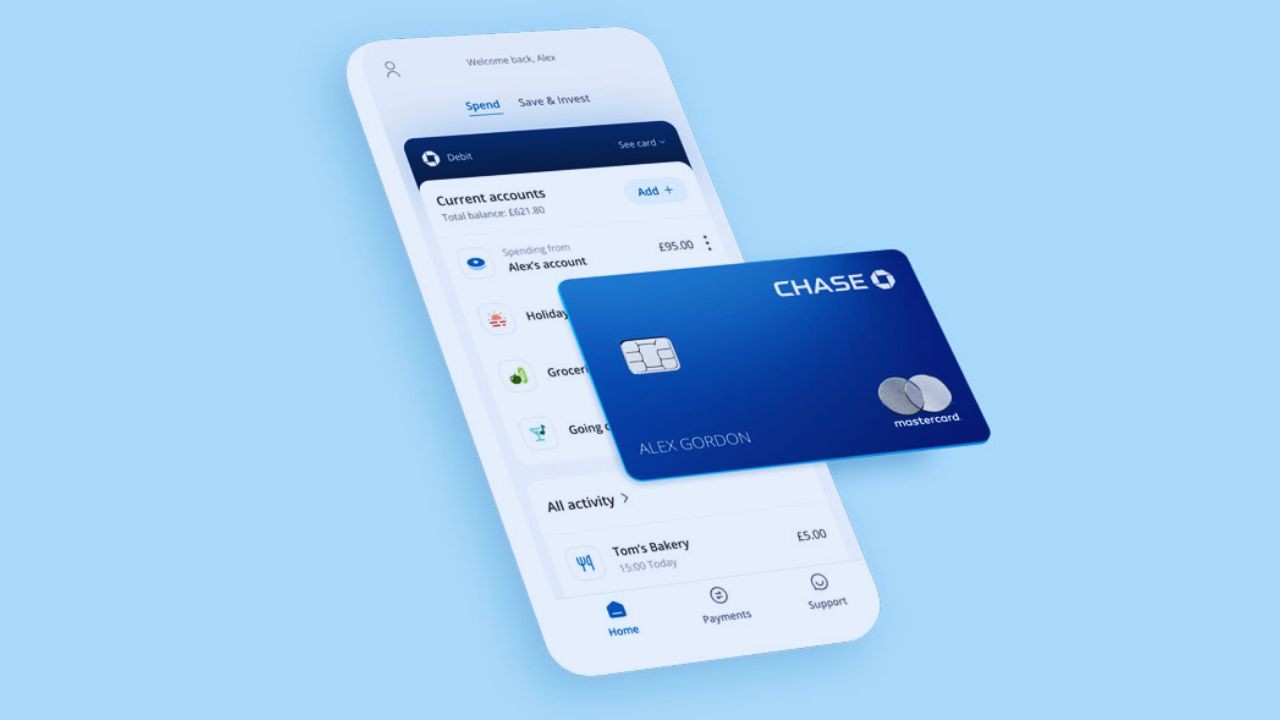

The Chase UK card has become an intriguing choice for those who want to earn cashback on all their daily spending. With 1% cashback on everything you pay for, this card is nudging many to rethink how they use their debit cards.

Whether you shop in supermarkets, dine out, or pay for streaming services, cashback can quietly build up.

This article explores what makes the Chase UK cashback card attractive, what to watch out for, and who is likely to benefit most.

It’s written for anyone curious about maximizing rewards from day-to-day purchases, especially if you want a straightforward, low-hassle setup.

What is the Chase UK Cashback Card?

The Chase UK card is a debit card linked to the Chase current account offered to residents in the United Kingdom. Unlike some credit cards, there’s no need to worry about credit checks for card spend, but the cashback model remains generous.

Many are surprised to see 1% cashback on almost every transaction—this includes shops, restaurants, bills, and many online subscriptions.

Some exceptions apply, and it’s wise to clarify these, but for the majority of everyday usage, rewards add up.

How Does the 1% Cashback Work?

Chase UK’s 1% cashback is paid automatically into your rewards section, available for transfer to your main account. There are a few typical requirements, such as needing an open Chase current account and being over 18 years old.

For the first year, this cashback model covers most spending, with monthly caps in some scenarios and a handful of non-eligible payments. There’s no complicated registration; simply use the card for your purchases.

Excluded Transactions

- Cash withdrawals at ATMs

- Buying foreign currency or traveller’s cheques

- Gambling-related transactions

- Some payment services

The full list can be checked on the Chase UK website for accuracy, since terms occasionally change.

How Cashbacks Are Paid Out

Once cashback accumulates, it’s visible in the Chase app under a separate rewards balance.

It’s possible to transfer this amount into your current account at any time, without waiting for a set date. Some users prefer to let it build up before cashing out—a personal choice, really.

Who Is Eligible for the Chase Card?

Chase UK accounts are available to UK residents aged 18 or over with an eligible ID and UK address. There’s no minimum income requirement, which helps keep this card accessible for students, part-time workers, and self-employed people.

Solely online account registration is standard (via the Chase app), so reliable access to a smartphone is necessary. The initial sign-up is generally quick, but as with any financial product, ID verification could take longer if documents aren’t clear.

Why Consider a 1% Cashback Debit Card?

The appeal is in its simplicity. No ongoing fees or interest rates to juggle, unlike many credit cards. For cautious spenders or people with credit aversion, a debit-based cashback system removes the worry about overspending or accruing debt.

One could argue the 1% rate is quite competitive, especially since many traditional debit cards offer no direct rewards.

Most UK consumers might see the biggest benefit just by using the card for regular spending like groceries, travel (excluding cash withdrawals), and entertainment.

Cashback vs Traditional Credit Card Points

There are subtle differences. Credit cards might offer higher headline rewards, but they often tie the best rates to particular retailers or require high spending thresholds.

For those preferring straightforward, universal cashback with no mental calculation, Chase UK stands out.

How to Get the Most Out of Chase UK 1% Cashback

If you’re wondering how to maximize your annual rewards, the approach can be very simple. The key idea: channel as much regular (eligible) spending through the card as practical, while avoiding overspending just to chase cashback returns.

It’s surprisingly easy to fall into that trap—maybe everyone has been tempted at some point.

Popular Spending Categories for Cashback

- Weekly groceries and household items

- Transportation costs (bus, tube, rail)

- Cafes, restaurants, and pubs

- Streaming subscriptions and app stores

- Utility bills (where accepted)

A quick check in the Chase app’s spending insights can help spot patterns and identify areas where it makes sense to prioritize the card.

Tips for Maximizing Value

- Set up recurring payments for monthly expenses through the card

- Watch for introductory offers and seasonal promotions

- Keep an eye on your monthly cap (if applicable) to avoid disappointment

- Review reward-eligible merchants periodically—categories sometimes shift

Even small purchases, like daily coffees or groceries, will gradually contribute to overall cashback totals. For many, it’s the consistency that matters, not dramatic one-off spending.

How Does Chase UK Compare to Other Cashback Cards?

The UK financial scene offers a handful of other cashback options, though most are credit cards.

Comparing Chase to these choices depends heavily on your personal habits—some credit cards offer higher returns for travel or specific retailers, but they usually demand a stronger credit profile and tend to come with various fees or strict eligibility rules.

Some major UK banks occasionally offer promotional cashback on select debit cards, but these will often be limited-time or restricted to narrow types of spending.

Understanding the Limitations and Potential Downsides

No product is flawless. For the Chase UK card, the cashback usually lasts for 12 months from account opening, after which the future rewards structure may change (the bank sometimes extends the cashback period, but this is not guaranteed).

Additionally, not every payment triggers rewards. As with many bank accounts, if your card is declined or misused, there could be additional blocks or even loss of cashback entitlement.

Some users experience the odd technical glitch with the app—nothing major, usually, but it sometimes happens.

The UK is still catching up to the US regarding widespread debit rewards, so this space remains a little unpredictable in terms of long-term benefit.

Account and Customer Service Insights

Chase UK is operated entirely online, so there are no physical branches to visit. Live chat and in-app support are the main avenues for help.

While many users report quick and friendly service, it remains a digital-first experience—which might not suit those who value face-to-face banking.

Is the Chase UK Cashback Card Safe and Secure?

Chase is a division of JPMorgan Chase, one of the world’s largest banking groups. UK customers’ funds are protected up to £85,000 by the Financial Services Compensation Scheme (FSCS).

The app includes several security features, including instant card freezing and customizable notifications for each transaction—a definite plus for peace of mind.

Data privacy and strong authentication policies make this account as secure as any leading UK challenger bank.

Common Questions about Chase UK 1% Cashback

Does the cashback expire?

Unclaimed cashback typically won’t expire if your account remains open and in good standing. Offers or terms could shift over time, so checking the latest from Chase is recommended.

Are there fees for the Chase UK card?

Currently, the account and debit card have no monthly or annual fees attached. Foreign exchange for overseas purchases is also fee-free at competitive rates—a nice bonus for regular travelers.

Can you stack cashback with other offers?

Some retailers provide their own loyalty points, which can be earned alongside the Chase cashback. However, stacking with other bank cashback schemes may not always work; check each program’s rules carefully.

Conclusion

The Chase UK Cashback Card offers simple 1% cashback on everyday purchases, helping users earn rewards effortlessly, manage spending wisely, and maximize savings through consistent, regular use.

Note: There are risks involved when applying for and using credit. Consult the bank’s terms and conditions page for more information.